Top ten things to know about migration

Net migration is having a huge effect on the New Zealand economy prompting debate and leading to policy changes. We’ve curated a list of the top ten things to know about migration in New Zealand.

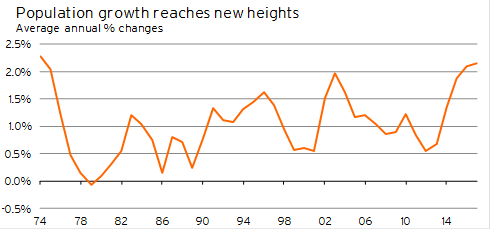

1. Population growth is at its highest since the 1970s

Net migration has been a powerful boost to New Zealand’s population in recent years. Back in June 2012, we were losing just over 3,000 people a year (mostly due to New Zealand citizens moving to Australia). Fast forward five years and we are gaining people at a rate of 72,305 every 12 months. This turnaround has pushed population growth to 2.14%pa – its fastest pace since 1974!

Graph 1

Population growth has been driven by both strong arrivals growth and low departure numbers. Over the year to June 2016, the number of people moving to New Zealand was 49% higher than in June 2013. Our buoyant economy, strong employment growth, and relatively accommodative migration policies have been big pull factors for migrants. These conditions, coupled with a clampdown on rights to social security services in Australia, have also encouraged more New Zealanders to stay on this side of the Ditch.

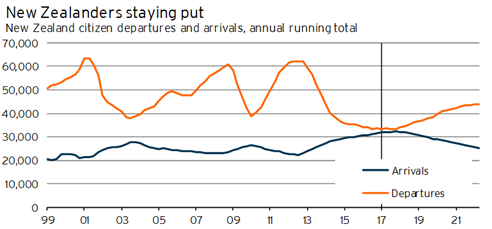

New Zealanders are a big swing factor in overall migration statistics .

Over the last three decades, the number of New Zealand citizen departures has varied between 25,000 and 60,000 a year. These figures mean that, typically, New Zealand citizens account for about 50% of total departures. But at around 33,000 departures in the year to June 2017, New Zealand citizen departures are at their lowest level since the early 1990s!

Graph 2

On the arrivals side, the number of New Zealand citizens coming in is at its highest level since at least the 1980s! And New Zealand citizen arrivals numbers are still climbing.

Conditions offshore make moving or remaining overseas look a lot less appealing than it once was. The New Zealand economy is in a strong growth position and is not faced with the political uncertainties or economic struggles that many countries are dealing with right now.

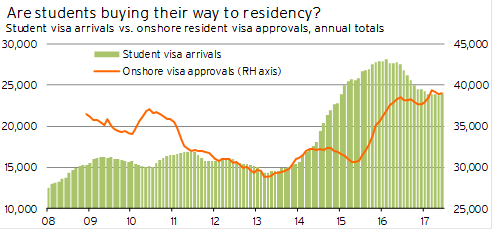

3. Students might be our future residents

Growth in student arrivals was integral to the initial lift in net migration back in 2013 and 2014. A rule change enabling students to work more while studying in New Zealand, along with a push from developing countries to promote a foreign education (eg in New Zealand) prompted a surge in student arrivals. In the March 2015 year, student arrivals had grown 52% – equivalent to more than 8,600 additional arrivals.

At the time, we cautioned that this lift in arrivals was unlikely to have the same effect on migration as a lift in resident arrivals. For the most part students weren’t expected to stay longer than the duration of their courses, and they weren’t expected to put down roots by buying a house. But we might have been wrong.

Although we do not have the data to confirm that migrants have used student visas as a “back-door” way to obtain residency, we are suspicious of the similar rise in resident visa applications that follows about a year after increases in student arrivals.

Graph 3

However, there has been a tightening of student visa requirements that has subsequently prevented a lot of would-be students from coming to New Zealand. In the year to June 2017, there were 23,983 people who arrived on student visas, with this number having declined 15% from its peak in early 2016. The slowdown was largely due to a tightening of English language testing requirements, targeting students with passports from countries who had previously low approval ratings.

Flat month-on-month growth rates suggest that the number of student visa arrivals has begun to stabilise and that we are moving toward a new equilibrium of student arrivals of around 23,000-24,000 a year.

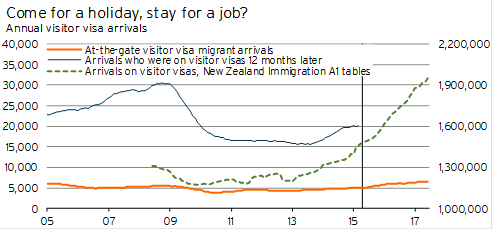

4. When the economy is doing well, tourists find jobs and stay

The recent boom in tourism could also provide additional impetus to population growth. Recent data from Statistics NZ shows that in the year to March 2015, an additional 15,000 tourists stayed in New Zealand long enough to be reclassified as permanent or long-term migrants. The data suggests that when the economy is hot, tourists tend to stay on in New Zealand as either students or workers.

Given our recent economic performance, the number of tourists staying in New Zealand for a longer period is likely to rise further.

Graph 4

Are we underestimating our migrant numbers ? provides a more detailed discussion on how many tourists and other people on temporary visas are staying in New Zealand for more than a year.

5. April rule changes will have a limited impact on arrivals

The full effects of rule changes to work and resident visas introduced in April are unlikely to show up in the migration statistics we normally look at. The new rules introduce remuneration thresholds for those wanting residency under the Skilled Migrant category and for those wanting to extend or reapply for their three-year Essential Skills work visa.

Both changes affect those wanting to stay in New Zealand long-term, and applicants are by-and-large already in the country. As a result, these rule changes will not create a sharp drop in at-the-gate arrivals, but are likely to force more people to leave New Zealand over time.

But the point of these rule changes is to concentrate the mix of migrants staying here long-term toward higher skill levels, with the intent of improving overall labour productivity and living standards in New Zealand.

6. But skills-based policy so far has had no impact

There is little evidence that New Zealand’s skills-based immigration policy of the last 25 years has led to improved productivity or living standards across the economy.1 However, changes to immigration policy last decade appear to have improved the integration of new immigrants into the labour force due to better occupational and skills matching.

7. Friends first, jobs second on migrant priority lists

Migrant networks are an important factor when foreign immigrants are choosing where to settle in New Zealand, despite this country’s skills-focused migration system.2 Labour market opportunities become a more important factor the longer that the migrants have been in New Zealand.

On average, 56% of foreign migrants (excluding New Zealanders and Australians) over the last 25 years have said they plan to settle in Auckland, which is an average of 23 percentage points above the region’s share of New Zealand’s population. In this regard, the fact that Auckland has a high proportion of immigrants potentially becomes self-reinforcing, placing stress on the region’s housing market, civil infrastructure, and education and health services.

8. Migration: good for Kiwi workers, not so much for migrants

Higher net migration inflows do not have a significant negative effect on employment or wage rates for NZ-born workers, but instead negatively affect the labour market outcomes of other recent migrants.3

Migrants to New Zealand face an initial entry disadvantage in terms of both their employment rates and wage rates compared with equivalent New Zealand-born workers . This disadvantage reduces over time for some immigrants. Less-skilled migrants tend to suffer continued lower employment and wage rates than comparable NZ-born workers, but these labour outcomes are still likely to be superior to the opportunities available in these migrants’ home countries.

The implied boost by migrants living and buying things in New Zealand appears to improve employment and wage rates for NZ-born workers, particularly those in the medium-skill subgroup.

Furthermore , there is no evidence that the increase in temporary migrants over the last 15 years has had a negative effect on labour market outcomes of New Zealanders. This conclusion continued to hold true in the wake of the GFC when the labour market softened but there was less downward adjustment in the employment of temporary migrants.

9. Research on the effects of migration on the New Zealand housing market is mixed

A lift in migration flows equivalent to 1% of the population could push up average house prices by between 6% and 12%, with the effects of an increase in arrivals greater than an equivalent decrease in departures.4 Returning New Zealanders have a greater effect on house prices than changes in the number of foreign immigrants.5 However, regional analysis suggests that much of the correlation between net migration and house price movements might be caused by other factors (such as economic growth or income growth), rather than there being a strong causal relationship between migration and house prices.

A lift in net migration might have a large positive effect on house prices in the short or medium-term due to delays in the response of the residential construction sector to increased demand for housing and/or more optimistic expectations about future property values.6 In our view, a lack of capacity in the construction sector because of very low levels of activity following the Global Financial Crisis suggests that the relatively limited response in residential building has been a significant factor in the house price boom of the last five years.

Although migration is helping to alleviate pressure in the labour market, it faces political headwinds. The rapid build-up in migrant inflows has put pressure on housing and infrastructure.

Migration’s effect on cost pressures can be seen in limited wage and price growth. But a sharp reduction in net migration probably won’t lead to as much of a lift in wage growth (or employment) as you’d think it might. If faced with rapidly increasing labour costs, businesses are likely to turn to automating processes as much as possible. We don’t think that automation is inherently a bad thing – improving productivity is one way to get more for your money – but we do think that “turning the tap off” on net migration will impose sharp disruptive change for many parts of the economy. As a result, we suggest a more progressive approach to toning down net migration, and to focus migration policy on those that are intending to stay in New Zealand long-term through indirectly or directly obtaining residency.

1 www.treasury.govt.nz/publications/research-policy/wp/2014/14-10/twp14-10.pdf

2 http://motu-www.motu.org.nz/wpapers/07_11.pdf

3 http://motu-www.motu.org.nz/wpapers/09_10.pdf

4 http://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Analytical%20notes/2013/an2013-10.pdf .

5 http://otu-www.motu.org.nz/wpapers/08_06.pdf

6 www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Discussion%20papers/2007/dp07-12.pdf